2017年3月17日

保険業界のIT革命「インステック」 PartⅠ

保険業での「フィンテック」技術の応用である「インステック」がすでに開始されている

おはようございます。

本日はイギリスのクオリティペーパーである「フィナンシャル・タイムズ」からの記事です。「ヘルステック」と「フィンテック」に隣接する「インステック」の記事です。

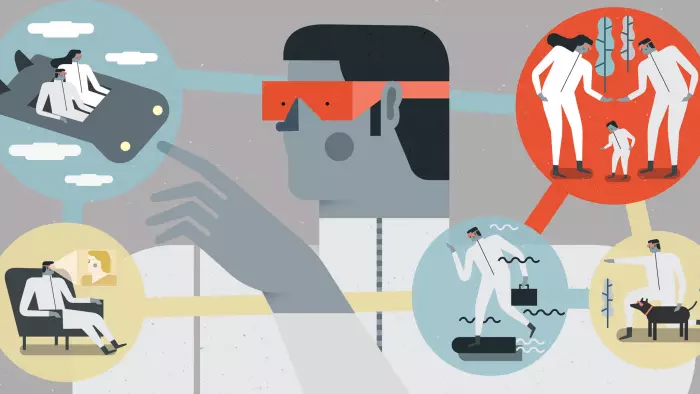

「インステック」 insurtech とは「インシュアランス・テクノロジー」 insurance technology の略で「保険テクノロジー」という意味です。保険業界と保険自体を大きく分解して、IT技術によって金融業のように、煩雑な手続きをなくし、「与信」にあたる「既往歴」などを正確に評価して、保険契約にかかる無駄をなくしていこうという試みです。

またフィンテックと同様、そこにはP2PやPSSという思想も大きく存在しています。保険のかけ方をより細かく効率的にするものです。現在日本のテレビCMでも「走った分だけ」という宣伝がなされていますが、あれこそまさに「インステック」を表したものといえます。年間保険料には無駄が多く、人間が何かをしているときにだけ保険をかけ、その必要のない時はそれを切る。それをAIが行うというものです。

保険業界は銀行と同じ金融業界なので、「フィンテック」やブロックチェーンの仕組みが適応しやすい領域だったのです。金融業界はATMの導入など早くから「フィンテック」技術が導入されていましたが、保険業界は人間の判断力、足を使った営業など、完全に人力の世界で、テクノロジーの入る隙間のない「伏魔殿」といわれてきました。

ところが、日本では「インステック」のほうが早くに実現しているようです。欧米や中国では暗号通過(クリプト・カレンシー)がすでに実際の物となっていますが、日本では現金がいまだに強く、そうそうなくなりそうな気配を見せません。ICカードの広まりやクレカ、その他の電子マネーの部分でしばらくとどまりそうです。(2020年のオリンピックまでにそのままというわけには絶対に行きませんが。)

しかし、保険の分野ではセンサ技術の進歩のおかげで「走った分だけ」保険を掛けることがすでに可能になっています。紙と人力の「伏魔殿」であった「インステック」が、日本での「テック」の広まりと協働消費という新しいシステムの入り口となるかもしれません。

そしてそれは医療業界とも密接に結びついています。つまり、当社の目指す「ヘルステック」普及のためには、保険業界や支払いシステムの変革がそれを大きく後押しするものだといえるのです。

保険とビッグデータ技術革命

新しい保険プラン加入のために際限のないほど大量の書類に記入することは、過去のものになるでしょう

Insurance and the big data technology revolution

Filling in endless forms to buy a new policy may become a thing of the past

February 24, 2017

by: Oliver Ralph

https://www.ft.com/content/bb9f1ce8-f84b-11e6-bd4e-68d53499ed71

© Tiago Gallo

自動カミソリ、ジェットパック、航空路での渋滞。ジェットソンズははるか未来の人生についてさまざまな予測をしました。しかし、1960年代と1980年代に作られたハンナ・バーベラの漫画は、保険の問題を無視して飛ばしていました。それはほとんど驚くべきことではありません。リスク管理は、SF小説ではあまり一般的な話題ではありません。そして、いずれにしても、保険業界は新しい技術を必ずしもすぐに手に入れてきたわけではありません。「業界全体は、5年または10年前の生活のあり方に目を向けています」とAvivaの最高技術責任者(CIO)Andrew Bremは語っています。

そのように感じているのは彼ただ一人だけではありません。保険仲介企業であるウィリス・タワーズ・ワトソンによる保険会社に対する最近の調査では、回答者の74%が業界がデジタル革新においてリーダーシップを発揮できなかったと感じていました。

しかし、今から20年後に加入する可能性のある保険は、今日私たちが必要としている保険とはかなり違って見えるという考えに保険業界が目覚めたら、変化が起こり始めるでしょう。

大手保険会社はイノヴェーションと研究に何百万ドルもの資金を投入しています。ブレム氏の会社は、新しいアイデアに取り組むためにロンドン東部のホクストンスクエアに「デジタルガレージ」と呼ばれるものを設置しました。Axaは、ITおよびデジタル開発に30億ユーロを超える投資しています。また、ヨーロッパのAllinanzとMunich ReからカナダのManulife、バミューダのXLCatlinなどの会社も多額の投資を行っています。

その一方で、大手企業に挑戦しようとしている、いわゆる「インステック」スタートアップ企業に、さらに数十億ドルが投入されています。 Uber、Airbnb、Netflix、Spotifyが他の業界で激変を起こしたのと同じように、So-sure、Friendsurance、Lemonade、Guevara、Brollyやその他多くの企業などが保険を破壊することを目指しています。CB Insightsによると、昨年、173件の取引で17億ドルが保険スタートアップ企業に投入されました。

オーストラリアと英国で活動するインステックのスタートアップ企業Trovを経営するScott Walchek氏は「保険は将来大きく変化するだろう。我々はテクノロジーがリスク管理に適用される出発点にいる」と語っています。

保険会社はすでにこれを試しています。昨年、AdmiralはFacebookの記事で使用されている言語を使って、ある人がどれだけ危険な運転をしているかを評価したいと思っていました。Facebookは実験を躊躇しましたが、業界の専門家によれば、同様に革新的な方法でデータを使ってリスクを評価しようとしている保険会社がほかにも存在します。

その結果、インステックの愛好家によれば、煩雑で時間がかかるアンケートで保険購入者に負担をかけることなく、正確に価格を設定するシステムが現れるでしょう。

価格比較アプリが保険を購入する手続きをいっそう楽にしている ©Alamy

保険購入方法

次の20年間で最初に変わる可能性のあるのは、保険を購入する方法です。価格比較サイトやモバイルアプリの開発でも、多くの人が購入までの経過に時間がかかり不満を感じています。

ブレム氏は「保険を購入することは、ばかばかしいほど時代に逆行しており、次から次へと質問された挙句に見積もりをだされる。これらの質問が基本的に不要な世界に我々は移行していくことになるでしょう。ビッグデータを使用することで、人々に質問することを必要としない、興味深く正確なリスクの予測因子を私たちは見出しつつあります」とBrem氏は述べています。

https://youtu.be/_5xzl_CobPI

すでに行われている例の1つは、Avivaによる自動車保険の価格設定方法です。 昔からこれには車の種類、場所、運転歴に関する多くの質問が含まれていました。しかし同社は、生命保険契約の購入とより安全な運転の間に統計的な関連性があることがわかっています。そのため保険契約者には、より低い見積り価格が提示されるのです。

この考え方は、今後数十年にわたって拡大していくでしょう。「そう遠くない将来、データの威力は(保険会社にとって)同じように見える人々が、もはや同じに見えなくなることを意味するのです」とBrem氏は語ります。ウィリスタワーズワトソンの調査では、回答者の94%が、今後5年間にテクノロジーによって一変するのは、販売であると答えています。

購入する保険

私たちが何に保険を掛け、どのように掛けるかは、根本的に変わる可能性があります。今日私たちは、自動車保険、住宅保険、旅行保険を買っています。これは数十年前とまったく同じですが、今ではネットでも保険仲介業者からでも買うことができます。

しかし、Walchek氏は、将来の保険プランは、今日の保険プランと似ているところはほとんどないと考えています。「私たちは依然として残したいものがあり、それのためにリスクを抱えています。変化したのは、生活とそのリスクがより正確に測定されているということです。以前は、たとえば、郵便番号を使用してリスクの兆候を示すことがありました。 今、それはフィートとインチで測定されています」と彼は語ります。最近何人かが氷で滑って転んだ道路を、ある人が歩いていこうとしていることを携帯電話の信号や他のセンサーが検出したと想像してください。保険会社は保険契約者がその道を歩いている間に、もっと注意深く歩くよう警告するメッセージを送信するか、保険料を自動的に引き上げて対応します。

より短期的には、保険の精度が高いほど、保険は破壊されていき、より理解しやすい内容に分けられていきます。年間保険料も、近くなくなっていくでしょう。

Trovは、限られた期間の特定保険項目の補償範囲をすでに提供しています。顧客は、例えばある1日の間カメラを補償する保険に加入することができます。

自動車保険にも同じ原則が適用されています。年間保険料のおかげで、人々は駐車場や私道で車に座っていることに生活の大半を費やしている車に、保険をかけている不満を誰もが持っています。保険のオン・オフを切り替えることができるというのは、普段は保険がいらないユーザーにとっては魅力的なものになるといわれています。英国のCuvvaと米国のMetromileも、シンプルな保険を提供している企業です。

しかし、誰もがこのモデルが普遍的な魅力を持っていると考えているわけではありません。KPMGの保険テクノロジー専門家Murray Raisbeck氏は「決めるのは消費者ですが、消費者は保険についてそれほど考えたくはないでしょう」。

Munich Re Digital Partnersの最高経営責任者Andrew Rearも同意します。「保険をかけたり切ったりしたいと思っている人はいません。しかし、保険業の細かな分解について興味深いことの1つは、顧客が保険のオンとオフを切り替える必要はないということです。 何かをしているときは保険をかけようと自分で決められるし、あなたがなにかをしているときは機械が判断して、保険適用をオンにするのです」。

もう一つの可能性は、現時点では、私たちがまったく保証していないものを保証するようになることです。「長期的には、保険料の変動が見られるでしょう」とリア氏は語ります。「センサ技術の影響でリスクが軽減し、保険料を削減することができる分野ではリスクが下がっていますが、新たなリスクや保険が必要な新しい分野もまた生まれます」。

デジタルデータが一つの例です。「画像のような仮想資産やゲームのアイテムのコレクションがあります」とBrem氏は言う。「デジタル世界は、多くの新しいタイプの資産を生み出しています。」

現時点では、サイバー保険が企業保険になる傾向があり、例えばデータ侵害による被害補償を行っています。しかし、現在デジタルで保有されている個人データの量を考慮して、一部の保険会社は、個人的なサイバー保険の市場が存在するかどうかの問題を検討し始めています。

編集部からのコメントです。

ここまでが前半です。長文記事ですので次回との二回に分けて掲載いたします。

英語原文です。

Automatic razors, jet packs and traffic jams on the skyways. The Jetsons made all sorts of

predictions about life in the distant future. But the Hanna-Barbera cartoon, made in the 1960s and

1980s, skipped over the question of insurance.

That is hardly surprising. Risk management is rarely a popular topic in science fiction. And in any

case, the insurance industry has not always been quick to pick up on new technology. “The entire

industry is focused on how life was lived five or 10 years ago,” says Andrew Brem, chief digital

officer at Aviva.

He is not the only one who feels that way. In a recent survey of insurers by broker Willis Towers

Watson, 74 per cent of respondents felt the industry had failed to show leadership in digital

innovation.

But change is coming as the industry wakes up to the idea that the cover we might buy 20 years from

now will look very different from the cover we need today.

Big insurance companies are pouring millions into innovation and research. Mr Brem’s company has

set up what it calls a “digital garage” in Hoxton Square in east London to work on new ideas. Axa is

putting more than €3bn into IT and digital developments. And others, from Allianz and Munich Re

in Europe to Manulife in Canada and XL Catlin in Bermuda, are also investing heavily.

Meanwhile, billions more are going into so-called “insurtech” start-ups which are aiming to

challenge the big players. The likes of So-sure, Friendsurance, Lemonade, Guevara, Brolly and a

host of others are aiming to disrupt insurancein the same way that Uber, Airbnb, Netflix and Spotify

have caused upheaval in other industries. According to CB Insights, $1.7bn went into insurance

start-ups last year, across 173 deals.

“Insurance will be enormously different in the future,” says Scott Walchek who runs Trov, an

insurtech start-up that operates in Australia and the UK. “We’re at the beginning of technology being

applied to risk management.”

Price comparison apps have made the process of buying insurance easier © Alamy

How we buy

The first thing that could change over the next two decades is the way we buy insurance. Even with

the development of price comparison sites and mobile apps, many people still find the experience

time consuming and frustrating.

“Buying insurance is ridiculously retrograde, with endless questions resulting in a quote,” says Mr

Brem. “We’ll be moving to a world where those questions are basically unnecessary. With the use of

big data, we are discovering interesting and accurate predictors of risk that do not involve asking

people questions.”

https://youtu.be/_5xzl_CobPI

One example already in use is the way that Aviva prices its car insurance. Traditionally, this involved

a lot of questions about the type of car, the location and the driving history. But the company has

found a statistical link between the purchase of life insurance policies and safer driving. So life

insurance policyholders get lower quotes.

This idea is likely to grow over the next couple of decades. “Not far into the future, the power of the

data will mean that people who look the same [to an insurer] now will no longer look the same,”

says Mr Brem.

Insurers are already experimenting with this. Last year, Admiral wanted to use the language used in

Facebook posts to gauge how dangerously a person would drive. Facebook got cold feet over the

experiment, but industry experts say that other insurers are likely to try to use data in similarly

innovative ways to assess risk.

The result, say insurtech enthusiasts, will be a system that accurately prices risk without burdening

the buyer with cumbersome, time-consuming questionnaires. In the Willis Towers Watson survey, 94

per cent of respondents said that distribution would be the area where technology would make the

biggest difference over the next five years.

What we buy

What we choose to cover, and how we choose to cover it, is also likely to change radically. Today,

we buy car insurance, home insurance and travel insurance that is much the same as it was a couple

of decades ago, except that we can now buy online as well as via a broker.

But Mr Walchek believes the policies of the future will bear little resemblance to those of today.

“We still own things that we want to protect and we take risks with them,” he says. “What has

changed is that life and its risk is being ever more precisely measured. In the past, for example, you

might use a postcode to give you an indication of risk. Now it is being measured in feet and inches.”

Imagine that mobile phone signals or other sensors detect that a person is about to walk down a road

where several people have recently fallen on ice, he says. The insurer will react by either sending a

message warning the person to walk more carefully or else automatically increase the premium and

cover while the policyholder is walking down that road.

In the shorter term, more precision is likely to mean that insurance will be broken down into easier

to digest chunks. The days of the annual policy may be numbered.

Trov is already offering coverage for specific items for limited periods of time. Customers can buy

insurance covering a camera for a day, for example.

The same principle is being applied to car insurance, where a common complaint is that, thanks to

annual policies, people are paying to insure cars that spend most of their lives sitting in car parks or

driveways. Being able to switch policies on and off, the argument goes, will make them much more

attractive to occasional users. Cuvva in the UK and Metromile in the US are among those offering

pared-down policies.

But not everyone thinks this model will have universal appeal. “The consumer has to make the

decision,” says Murray Raisbeck, an insurance technology specialist at KPMG. “But consumers

don’t really want to think about their insurance.”

Andrew Rear, chief executive of Munich Re Digital Partners, agrees. “I can’t see people wanting to

turn their insurance on and off. But one of the things that’s interesting about atomisation is that the

customer doesn’t have to turn the insurance on and off. You can make a decision that you want

insurance when you are doing X, and the machine decides when you are doing X [and so switches

the cover on].”

Another possibility is that we will be insuring things that, currently, we do not insure at all.

“Over the long term what we’ll see is a shift in insurance premiums,” says Mr Rear. “You see risks

going down in areas where sensor technology can make a difference and help to reduce risk and

reduce premiums, but you also get new risks and new sectors that need insuring.”

Digital data are one example. “There are virtual assets such as images, or collections of items in

games,” says Mr Brem. “The digital world is creating a lot of new types of assets.”

At the moment, cyber insurance tends to be a corporate policy, covering companies for the

consequences of a data breach, for example. But, given the amount of personal data that is now held

digitally, some insurers are starting to look at the question of whether there would be a market for

personal cyber cover.